What are Split Mortgages?

Wednesday 15 July, 2026

How Split Mortgages Work and Whether They Could Be Right for You

With mortgage rates, household budgets and financial planning remaining important topics for homeowners across the UK, more people are asking about split mortgages and whether they could offer greater flexibility than a traditional mortgage arrangement.

A split mortgage allows borrowers to divide their mortgage borrowing between different mortgage products, often combining a fixed-rate mortgage with a variable or tracker mortgage. This approach can provide a balance between payment security and the potential to benefit from future interest rate movements.

However, as with any mortgage decision, there are advantages, disadvantages and important considerations to understand before proceeding. Seeking professional mortgage advice can help ensure you fully understand your options and make an informed decision that is suitable for your circumstances.

Hayley Croft, Mortgage Broker, Lichfield, Staffordshire said:

“A split mortgage can be a useful solution for some borrowers who want a combination of certainty and flexibility. However, it is important to understand that there is no one-size-fits-all answer. What works well for one household may not be appropriate for another. Professional mortgage advice can help you understand the risks, benefits and alternatives before making a commitment.”

What Is a Split Mortgage?

A split mortgage is a mortgage arrangement where the total borrowing is divided into two or more separate mortgage products.

Each part of the mortgage will have its own interest rate, terms and monthly repayment calculations. Some lenders allow borrowers to split their borrowing between different products from the outset, while others may create split mortgage arrangements when borrowers move home and port an existing mortgage while taking additional borrowing on a separate product.

Why Are More Households Asking About Split Mortgages Now?

Several factors have contributed to increased interest in split mortgages:

- Ongoing uncertainty around future interest rates.

- Households looking for greater control over monthly budgeting.

- Borrowers wanting some protection from rate increases while still retaining the opportunity to benefit if rates fall.

- Increased awareness of alternative mortgage structures through mortgage advisers and financial education resources.

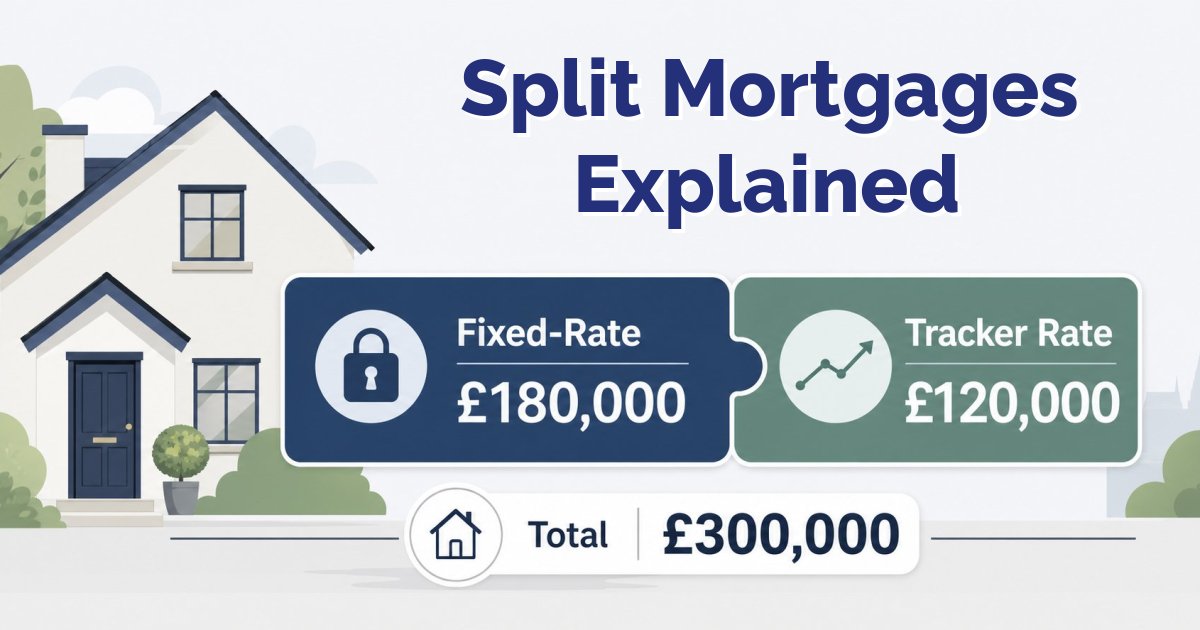

Example of a Split Mortgage

To illustrate how a split mortgage may work, consider a borrower with a £300,000 repayment mortgage.

They decide to split the borrowing as follows:

Fixed-Rate Portion

- £180,000 fixed for five years

- Monthly payment remains unchanged during the fixed period

Tracker Mortgage Portion

- £120,000 on a tracker rate

- Monthly payments can increase or decrease depending on movements in the underlying rate

If interest rates remain unchanged, the borrower continues making their combined monthly payments.

However, if interest rates fall, the tracker portion could become cheaper, reducing overall mortgage costs. Conversely, if rates rise, payments on the tracker portion could increase while the fixed-rate portion remains unchanged.

It is important to remember that actual repayment amounts will vary depending on the loan size, mortgage term, interest rates and lender criteria.

The Potential Benefits of a Split Mortgage

A Balance Between Security and Flexibility

Borrowers are attracted to split mortgages because they offer a combination of certainty and flexibility.

The fixed-rate element can provide reassurance that part of the mortgage payment will remain stable, while the variable portion may allow borrowers to benefit if interest rates fall.

Diversification of Interest Rate Risk

Rather than committing entirely to either fixed or variable rates, borrowers spread their exposure across different mortgage products.

Potential Overpayment Flexibility

Some variable-rate products allow greater overpayments or have fewer restrictions than fixed-rate products, although this will depend on the lender and mortgage terms.

Tailored Financial Planning

A split mortgage can sometimes be structured around individual circumstances, future plans and risk preferences.

The Potential Drawbacks of a Split Mortgage

Greater Complexity

Managing multiple mortgage products can be more complicated than having a single mortgage arrangement.

Different parts of the mortgage may:

- End on different dates

- Have different repayment terms

- Have different early repayment charges

Potentially Higher Fees

Depending on the lender, borrowers may incur separate product fees or arrangement fees for each mortgage portion.

Interest Rate Risk Remains

Although part of the borrowing may be protected by a fixed rate, the variable portion remains exposed to future interest rate increases.

Remortgaging Can Be More Complex

When product periods end at different times, borrowers may face more decisions regarding refinancing or switching mortgage products.

Who Could Use a Split Mortgage?

A split mortgage may be considered by:

- Home movers

- Remortgaging homeowners

- Borrowers with stable incomes who can accommodate some payment fluctuations

- Individuals seeking a balance between certainty and flexibility

- Borrowers who want to diversify their exposure to interest rate movements

Eligibility will depend on lender criteria, affordability assessments and individual circumstances.

Not all lenders offer split mortgage arrangements, and product availability can vary significantly. Split mortgage suitability will depend on individual circumstances

What Should You Consider Before Choosing a Split Mortgage?

Before proceeding with a split mortgage, it is important to consider:

Your Budget

Could you comfortably afford higher payments if interest rates rise on the variable portion?

Your Appetite for Risk

Some borrowers value certainty above all else, while others are comfortable accepting a degree of interest rate fluctuation.

Future Plans

Are you planning to move home, remortgage or make significant overpayments during the mortgage term?

Product Fees and Charges

Consider all costs associated with the arrangement, including fees and potential early repayment charges.

The Overall Cost

The cheapest-looking rate may not necessarily produce the lowest overall borrowing cost once fees and future rate movements are considered.

Are There Other Ways to Split a Mortgage?

A formal split mortgage is not the only option available.

Depending on your circumstances, alternatives may include:

Separate Mortgage Accounts

Some homeowners end up with separate mortgage products when porting an existing mortgage to a new property and taking additional borrowing.

Fixed-Rate Mortgage Only

Many borrowers choose the certainty of fixing their entire mortgage payment for a defined period. Fixed-rate mortgages remain the most common mortgage type in the UK.

Tracker or Variable Mortgage Only

Some borrowers are comfortable accepting payment fluctuations in exchange for the possibility of benefiting from future rate reductions.

Offset Mortgages

For suitable borrowers, offset mortgages may provide another way of managing borrowing costs while retaining access to savings.

The Importance of Professional Mortgage Advice

Choosing a mortgage involves more than simply comparing interest rates.

A mortgage adviser can help assess:

- Your affordability

- Your future plans

- Your attitude towards risk

- Available lender options

- Product fees and charges

- The overall suitability of a mortgage arrangement

Professional advice can help ensure that any recommendation is appropriate for your circumstances and objectives.

Final Thoughts and Considerations

A split mortgage can offer an attractive balance between stability and flexibility, particularly for borrowers who are unsure whether to commit entirely to a fixed or variable rate arrangement. However, it is not the right solution for everyone.

The additional complexity, potential fees and ongoing exposure to interest rate changes mean that careful consideration is essential. Before making any decision, it is important to understand how the arrangement would work in practice, how it may affect your monthly payments and whether alternative mortgage options may be more suitable.

Speaking to a qualified mortgage adviser can help you explore all available options and make an informed decision based on your personal circumstances, financial goals and long-term plans.

Please note: As a mortgage is secured against your home, it may be repossessed if you do not keep up the mortgage repayments. This article provides general information only and does not constitute mortgage, financial or legal advice. Mortgage products are subject to status, affordability assessment and lender criteria. A split mortgage does not guarantee lower repayments or reduced borrowing costs. The suitability of any mortgage arrangement will depend on your individual circumstances.

Latest News Previous Article